Medicare Part D in 2025: What’s Changing and Why It Matters

The Inflation Reduction Act (IRA), signed into law on August 16, 2022, introduced several important changes to Medicare with the goal of reducing healthcare costs for Medicare beneficiaries. The act primarily focuses on aspects such as prescription drug price negotiations, capping out-of-pocket costs for medications, and enhancing coverage for vaccines. The changes have been gradually implemented over the past few years, but the most significant are set to begin in 2025, with major adjustments that will impact both stand-alone Part D Plans and Medicare Advantage Prescription Drug Plans.

What’s Happened So Far

In 2023, the first wave of changes included a $35 monthly cap on out-of-pocket insulin costs and an expansion of coverage to include more Part D vaccines - specifically shingles and the flu - at no cost to Medicare beneficiaries. In 2024, Medicare expanded its drug price negotiations to include a wider range of high-cost medications. Additional adjustments were made to further lower prescription drug costs and out-of-pocket expenses, including the expansion of low-income cost-sharing and premium subsidy eligibility as well as a $0 copayment if a beneficiary reaches the Catastrophic Phase (more on that below).

Understanding Part D Phases

In order to understand Medicare Part D and the upcoming 2025 changes, it’s important to notice that the structure is different than, say, a Group Health Plan that you might get through an employer. Historically, there have been four distinct Part D Phases:

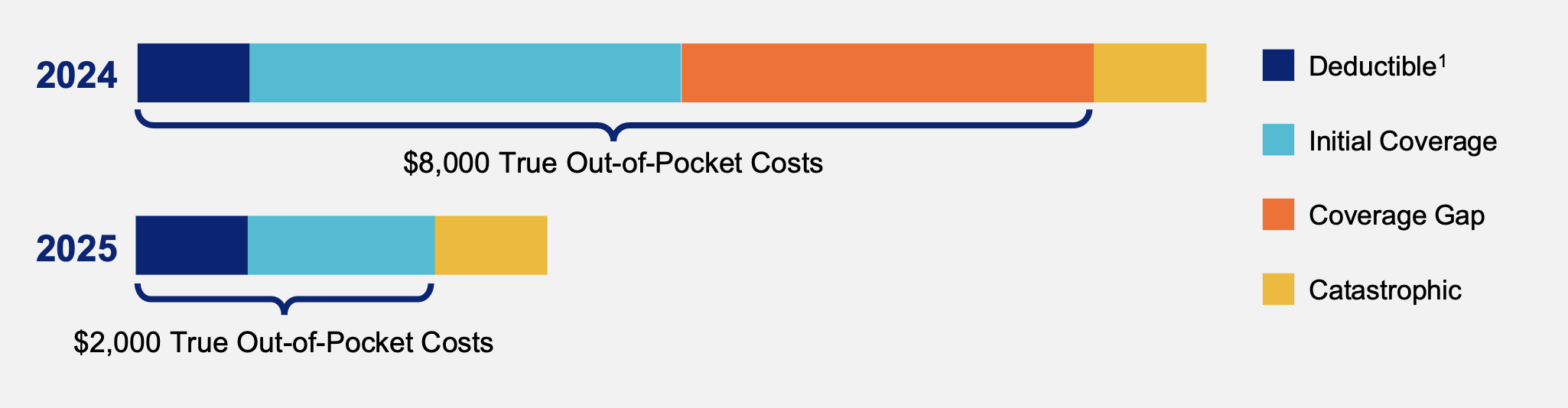

Deductible Phase - Enrollee pays all drug costs up to a set deductible amount ($545 in 2024), if applicable, before the plan begins to contribute. Note: Not all plans have an Rx deductible.

Initial Coverage Phase - After meeting the deductible, enrollees enter the Initial Coverage Phase where the plan contributes to covering drug costs and the enrollee pays a co-payment or co-insurance until the total drug costs reach a certain threshold - $5,030 in 2024.

Coverage Gap AKA The “Donut Hole” - Once out-of pocket costs exceed $5,030, enrollees enter the Coverage Gap - AKA the Donut Hole - where the drug plan contributes and the manufacturer offers a discount on brand name drugs. In this phase, the enrollee is responsible for paying a percentage of drug costs (25% in 2024) for both brand-name and generic drugs. Once the out-of-pocket expenses reach a certain threshold - $8,000 in 2024 - the enrollee enters the Catastrophic Phase. Only about 10% of enrollees enter the Donut Hole.

Catastrophic Phase - Once out-of-pocket costs exceed $8,000, the enrollee enters the Catastrophic Phase. The Part D plan and Medicare (coupled with the Manufacturer Discount Program) covers the cost of prescription drugs and starting in 2024, the enrollee pays $0. Only about 1% of enrollees enter the Catastrophic Phase.

What Will Happen in 2025

2025 will introduce some major changes to the Part D program, including:

Elimination of the Coverage Gap (Donut Hole) & Reallocation of Costs in the Catastrophic Phase

$2,000 Maximum on TrOOP (enrollees’ out-of-pocket drug cost)

Elimination of the Donut Hole & Reallocation of Costs in the Catastrophic Phase

In 2025, the Donut Hole will be eliminated, leaving just three Part D Phases. With the elimination of the Donut Hole, the cost responsibilities in the last phase - the Catastrophic Phase - will shift. In this phase, Medicare will pay a smaller portion (20% vs. 80% in 2024) and the Part D plans will be responsible for paying a higher share of the costs (60% vs. 20% in 2024). Enrollees will still pay $0 in the Catastrophic Phase.

How Could This Change Affect You? Members who typically reach the Donut Hole may significantly benefit from lower out-of-pocket costs in 2025. Although the exact impact on premiums will vary based on individual plans, it’s expected that the changes will result in higher premiums for beneficiaries as Part D plans look to cover the increased share of costs.

Source: United Healthcare

$2000 Maximum on TrOOP

In 2025, there will be a new $2,000 annual true out-of-pocket maximum (TrOOP), which is reduced from $8,000 in 2024. TrOOP is the out-of-pocket drug cost that accumulates during the Deductible and Initial Coverage Phases (think deductibles, coinsurances, other payments made on the beneficiaries behalf like State Pharmaceutical Assistance Program payments, etc). Premium payments do not count toward TrOOP. The Part D Plan will calculate the TrOOP behind the scenes to determine when a member will move to the Catastrophic Phase (As previously mentioned, enrollees pay $0 in the Catastrophic Phase).

Let’s look at an example: if a beneficiary's drug costs are $10,000 while in the Donut Hole, they would have previously paid 25% of these costs ($2,500). With the elimination of the Donut Hole, once an enroll reaches the $2,000 cap, they will now move directly to the Catastrophic Phase and will pay $0.

How Could This Change Affect You? Members may reach the Catastrophic Phase more quickly (where they will have no drug cost responsibility) due to the elimination of the Coverage Gap and the lower TrOOP of $2000.

Source: United Healthcare

The Deductible phase is only applicable if the plan includes a Rx Deductible in the plan design. Not all plans include a Rx Deductible.

Medicare Prescription Payment Plan

Due to the multiple phases in Part D prescription drug plans, the cost of prescriptions can fluctuate significantly throughout the year. Beginning in 2025, CMS has introduced the Medicare Prescription Payment Plan (sometimes referred to as “Smoothing”) offering members the option to pay $0 at the point-of-sale, and instead, pay for their prescriptions through a monthly payment program during the calendar year. Beneficiaries will need to “opt in” through their Medicare Part D plan provider.

How Will This Change Affect You? The Medicare Prescription Payment Plan allows beneficiaries to spread their prescription drug costs over monthly payments, making budgeting easier. While this plan does not reduce the total cost of medications, it can help manage expenses more predictably throughout the year.

For more info on the Medicare Prescription Payment Plan, visit cms.gov.

Summary:

In 2025, Medicare Part D will undergo major updates as a result of the Inflation Reduction Act. These changes aim to lower prescription drug costs and simplify payments. As you prepare for these updates, understanding how they impact your premiums and out-of-pocket expenses is crucial.

While it’s always recommended that you review your coverage annually with a Licensed Broker who specializes in Medicare, it’s even more important leading up to 2025. Speaking to a professional and planning ahead can help you make the most of your benefits and prevent unexpected costs. Annual Enrollment Period is October 15th-December 7th. Contact us today to review your plan at NO COST!

Care Compass is an independent insurance agency that helps seniors navigate the complexities of Medicare and other Senior Products. Our services are offered at no cost. Care Compass is proudly owned and operated in Blair County, Pennsylvania. We provide Medicare insurance assistance to the residents of Altoona, Hollidaysburg, Duncansville and the surrounding region.